The Volatility-Regime Reversion Archetype: Fading a Deviation Only When the Volatility Regime Supports Reversion

How a reusable method component fades a market-state deviation back toward its reference, but only while a separate volatility-regime read says the environment is one in which reversion works.

What the Volatility-Regime Reversion archetype is

A Volatility-Regime Reversion model is a reusable method component, not a fixed algorithm and not a single symbol or model. It measures how far a market-state reading has deviated from a reference level it tends to return to, then acts only when two things are true at once: a deviation is present, and a separate volatility-regime read classifies the current environment as one in which reversion works. The deviation says there is something to fade. The regime read decides whether fading it is sensible right now. Neither part is the full signal by itself; the decision is the conjunction of the two.

Throughout this explainer the input is described only as a masked market-state reading with a reference level. The public contract is the fade-toward-reference mechanism and its volatility-regime gate, not the proprietary input behind it. The archetype is the reusable component from which individual symbols and models are derived; it is not itself a prediction about any market.

The reversion premise: a deviation from a reference level

Reversion is a bet about distance closing. The archetype watches a market-state reading that has a reference level, a mean, an equilibrium, or a fair value, that the reading tends to return to over time. When the reading sits far from that reference, the archetype treats the gap as a deviation worth fading: it expects the reading to move back toward the reference rather than to keep stretching away.

The input must therefore be a quantity with a level it tends to return to, a spread, a residual, or a contained state. A raw price has no such fixed level, so it is not a valid input here. The reference is computed on a trailing window of the input's own past only; using the full sample would leak future information into the present, so the window is strictly trailing.

Why a deviation alone is not the full signal

A deviation reports distance from the reference, and distance alone. It says how far the reading has stretched, but it does not establish that the reading is about to snap back. A rule that fades every deviation, taking the opposite side of every stretch, fades straight into trends and breakouts, because the widest deviations often occur precisely when the environment has shifted and the reading is going to keep moving, not revert.

What separates a deviation that reverts from a deviation that runs is the volatility environment around it. In a calm, contained environment, a stretched reading tends to be pulled back. In an environment where volatility is expanding, the same stretch is more likely the start of a directional move that widens further. So the deviation is necessary but not sufficient. It identifies a candidate; it does not establish that the candidate is one to trade. That second judgment belongs to a separate component.

What the volatility-regime read does

The volatility-regime read is a separate, independent classifier that labels the current environment as either supportive of reversion or hostile to it. It reports the state of volatility itself, described in family terms only: whether volatility is contained and steady, in which case stretched readings tend to be pulled back, or expanding and unsettled, in which case stretched readings tend to keep running. Its single job is to grant or withhold permission to fade a deviation.

The regime read is a veto, not a vote. It never generates a trade on its own and it never adds to a directional score. It only withholds permission. When a deviation is present and the regime is supportive, the setup is tradable. When a deviation is present but the regime is hostile, there is no trade. This pairing, a deviation from a reference combined with a volatility-regime veto, is the component that defines the archetype.

How the archetype produces long, short, and flat

The decision follows a three-state contract built from the sign of the deviation plus the regime read. When the reading sits below its reference by enough to count as a deviation and the regime is supportive, the model takes the long side, fading the low reading back toward the reference. When the reading sits above its reference by enough and the regime is supportive, the model takes the short side, fading the high reading back toward the reference. In every other case the model is flat: either there is no meaningful deviation, or there is a deviation but the regime is hostile.

The sign of the deviation sets the side, and the regime read sets whether any side is taken at all. There is no separate trend model and no extra direction score; the same reference structure covers both directions, and the volatility regime decides whether either side is permitted.

Signal generation

Signal generation is deterministic and has no extra scoring layer. The model reads the current input, measures its deviation from the trailing reference, checks whether that deviation is large enough to count, reads the volatility regime, and maps the result to a target position of long, short, or flat. Read input, measure deviation, read the regime, gate, then position: the path from observation to action is short enough to trace by hand, which is what makes models of this archetype straightforward to monitor and to fault-find.

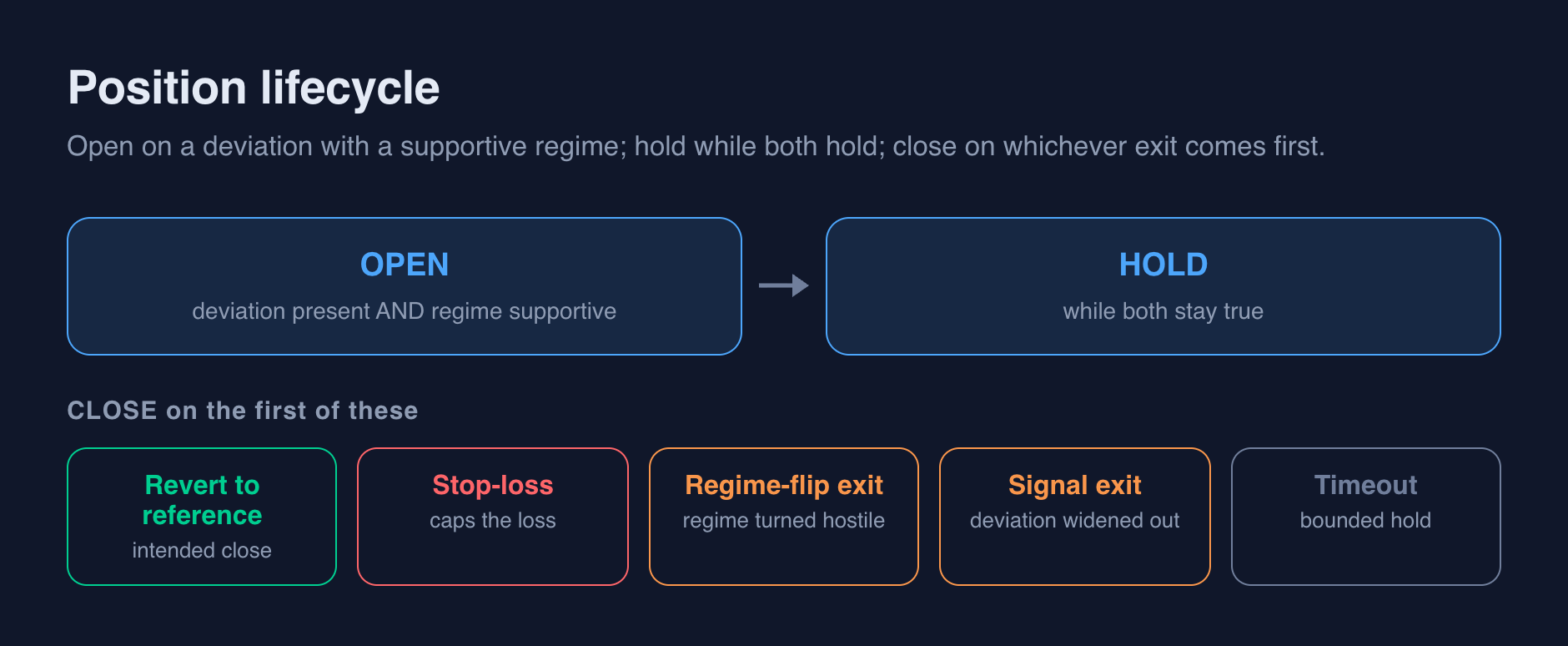

Position behaviour and lifecycle

A position has a simple lifecycle. It opens when a deviation is present and the regime is supportive. It is held while the deviation persists and the regime stays supportive. It closes on whichever of five events comes first.

The first and intended close is revert-to-reference: the reading returns toward its reference level, which is the outcome the fade was designed to capture. The remaining four are protective. A stop-loss caps the loss if the reading stretches further against the position. A regime-flip exit closes the position when the volatility regime turns hostile while a position is open, because the condition that justified the trade is gone. A signal exit closes the position when the deviation widens out of its tradable band without reverting. A timeout serves as a backstop so no position is held without bound. The mix of which exit ended each position is a compact summary of how a model actually behaved.

Risk controls

Risk control in this archetype is structural, baked into the mechanism, not applied by discretion after the fact. Six constructs each bound a distinct risk:

- The stand-aside flat state keeps the model out of the market whenever the two conditions are not met.

- The regime veto blocks fades whenever the volatility environment is hostile to reversion.

- The stop-loss caps the loss on any single position.

- The signal exit closes a position whose deviation widens out of the tradable band instead of reverting.

- The regime-flip exit releases a position the moment the volatility regime turns hostile.

- The timeout prevents a position from being held without bound.

This explainer describes a reusable method component, not a live model, not trading advice, and not a guarantee of future results. Backtests are described gross of commission and slippage unless explicitly netted.

Why the archetype stands aside

Standing aside is a first-class state, not a gap in coverage. There are two distinct flat cases. In the first, there is no meaningful deviation: the reading sits near its reference, so there is nothing to fade. In the second, a deviation is present but the regime is hostile: the reading is stretched, but the volatility environment is one in which reversion tends to fail, so the model takes no position.

Because both conditions must hold to open a trade, models of this archetype can be flat a large share of the time, and in particular through the volatile, trending stretches where fading is most dangerous. That is expected and desired. Continuous exposure would mean either the deviation band or the regime read was set too loose; long flat stretches through hostile regimes are evidence the component is being selective where it matters most.

Failure modes

Several failure modes follow directly from the mechanism:

- False reversion: a reading stretches far and is faded, but the deviation keeps widening because the move was a genuine breakout rather than a temporary dislocation, so the position loses.

- Regime read too loose: the regime rarely vetoes, so the model fades into expanding volatility and drifts back toward the naive fade-every-deviation rule, surrendering the selectivity the regime read was meant to provide.

- Regime read too strict: the regime confirms so rarely that the model starves and takes too few trades to evaluate.

- Volatility-read lag: because the regime is read from recent behaviour, it can label an environment supportive just as volatility begins to expand, so the worst fades cluster at the turn.

- Regime whipsaw: a regime read that flips quickly between supportive and hostile opens and closes positions in fast succession, paying costs without capturing reversion.

- Overfit reference or regime: a reference, a deviation band, or a regime threshold tuned to past conditions will not generalize to a new window.

These modes are inherent to the design and are meant to be measured and tolerated, not engineered away by tuning to one window.

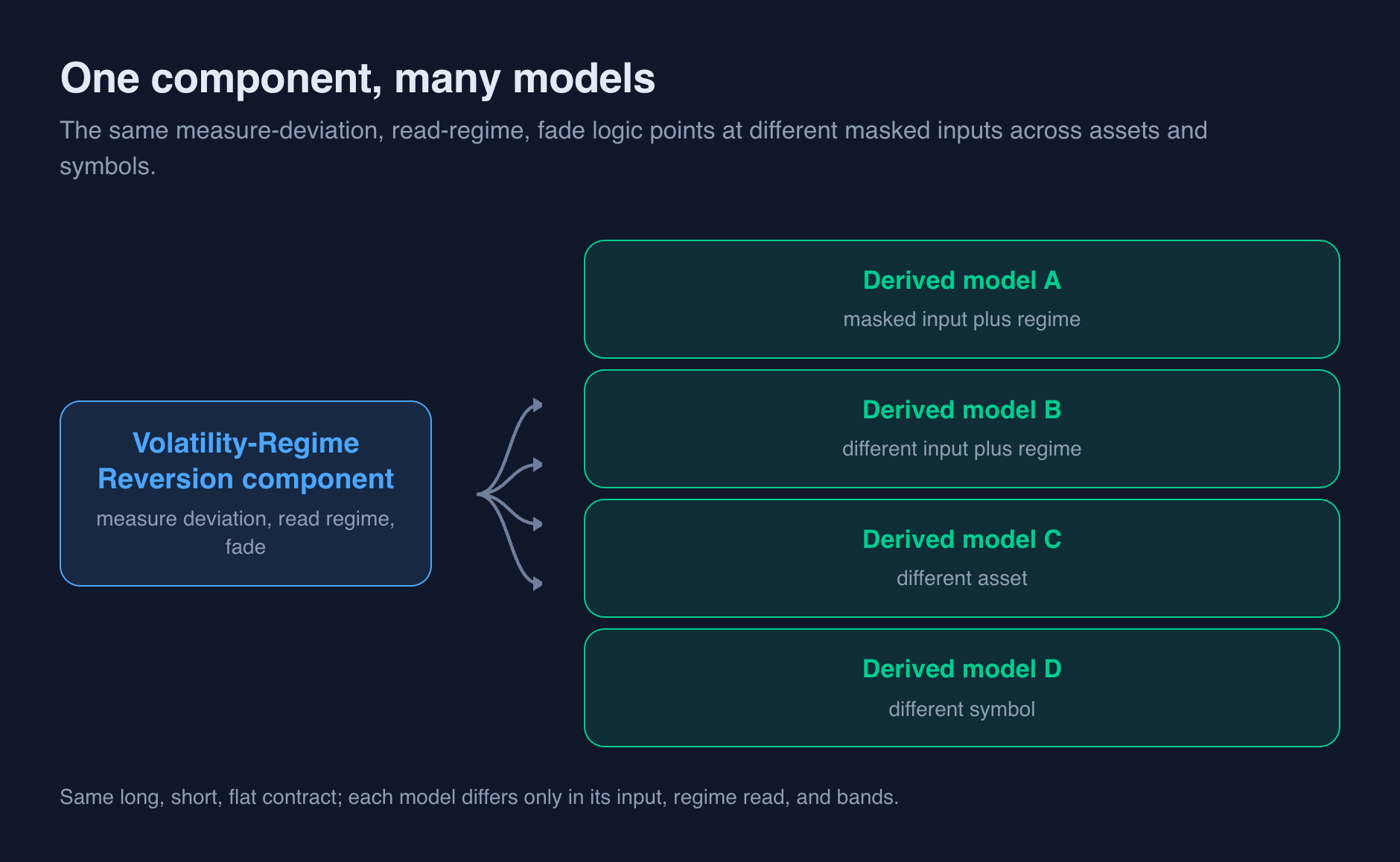

Why it is reusable across assets, symbols, and models

The archetype is a component rather than a one-off because its decision logic is independent of the specific input it consumes. The measure-deviation, read-regime, fade procedure can point at different masked inputs, each paired with its own reference and its own volatility-regime read, across different assets and symbols, to derive many distinct models. Every reading is measured against its own trailing reference before any decision is made, so the same mechanism transfers cleanly across inputs that share no common scale.

Each derived model inherits the same long, short, and flat contract and the same exit set. The models differ only in three things: which input they fade, how the volatility regime is read for that input, and where the deviation band and regime strictness are set. One component, many models, which is exactly why the archetype is defined separately from any model built from it.

Selecting a model of this archetype

A model built from the archetype is only a candidate until it clears the canonical acceptance bars. The same bars apply to every model of this shape: a minimum win rate, a minimum total return, a minimum average return per trade, a maximum drawdown ceiling, and a minimum sample size. These are generic selection criteria, not the record of any one model, and a candidate that misses any bar does not clear review for deployment. Once a model is deployed, it is measured against a buy-and-hold benchmark, so its edge is judged net of simply holding the asset.

Where the reference, bands, and regime read come from

The deviation band and the regime's strictness are the archetype's tuning surface. A wider deviation band makes the model more selective and keeps it flat more often; a narrower band makes it commit more readily and trade more often. The regime read's strictness works the same way: a stricter read confirms fewer environments as supportive, a looser read confirms more, and a looser read in particular is what lets fades leak into hostile, expanding volatility.

The reference, the deviation band, and the regime read must all be calibrated on a trailing window only. Tuning any of them to the whole record uses information that would not have been available at decision time, which is look-ahead and produces an overfit that will not survive a new window.

What the archetype deliberately omits

The archetype is defined as much by what it leaves out as by what it includes. There is no trend overlay, no second directional model, and no discretionary override. The only volatility handling is the regime gate itself; there is no separate volatility filter layered on top of it. Anything that cannot be expressed as a deviation from a reference combined with a supportive volatility regime is, by construction, outside the archetype. A model that needs a trend filter, a second confirming signal, or hand adjustment is a different archetype, not a tuned version of this one. Each omission keeps the path from observation to position auditable.

How to read a model built from it

To read a model derived from this archetype, work through the mechanism rather than a single headline number. Ask how the volatility regime is read and how often it vetoes an otherwise-tradable deviation. Ask whether the long and short sides are balanced or whether one dominates. Ask where positions close, the exit mix across revert-to-reference, stop-loss, regime-flip exit, signal exit, and timeout, since a high share of regime-flip exits says the regime read is doing real work. Ask how much of the time the model spends flat, and whether the flat stretches line up with hostile regimes. Then ask the decisive question: whether the veto rate and the exit mix hold up out-of-sample, or whether they were artifacts of the window the model was tuned on.

Archetype is not a symbol or a model

The archetype names how a model decides: measure a reading's deviation from its reference, and fade that deviation only while a volatility-regime read says the environment supports reversion. It does not name which market a model trades, and it does not fix how a model behaves over time. A model's behaviour label, whether it reads as trend, transitional, or mean-reversion, and its horizon are assigned per model from observed results, not inherited from the archetype. Two Volatility-Regime Reversion models on different inputs and regime reads can land in different behaviour labels while sharing the identical decision mechanism. The archetype is the reusable component; symbols and models are what you derive from it.

Conclusion

The Volatility-Regime Reversion archetype is a single-input, two-condition method component: measure a market-state reading's deviation from its reference, then fade that deviation only while a separate volatility-regime read says the environment supports reversion. Its strengths, real selectivity and a flat state that engages exactly through the volatile stretches where fading fails, and its weaknesses, a regime read set too loose or too strict, volatility-read lag, regime whipsaw, and a false reversion into a breakout, follow directly from that design. Because the decision logic is independent of the input it reads, the same component derives many models across many assets and symbols, each judged on its own against the canonical acceptance bars.

Key Takeaways

- The decision is a conjunction: a deviation from the reference AND a supportive volatility regime produce a trade; either condition alone produces flat.

- A deviation reports distance from the reference, not whether it will revert, so a separate volatility-regime read is required to make a deviation tradable.

- The regime read is a veto, not a vote: it withholds permission in hostile volatility and never generates a trade on its own.

- The sign of the deviation produces both sides: below the reference is long, above the reference is short, everything else is flat.

- Positions close on one of five exits, revert-to-reference, stop-loss, regime-flip exit, signal exit, or timeout, and the exit mix summarizes behaviour.

- An archetype is the reusable component from which symbols and models are derived; it is not itself a symbol or a model.

Next Steps and Further Research

- Derive and compare several models from this archetype, varying the input and the volatility-regime read, to separate archetype-wide behaviour from model-specific behaviour.

- Track the regime veto rate and the five-way exit mix as standard diagnostics for every model built from this archetype, and confirm both hold up out-of-sample.

- Stress-test the reference, the deviation band, and the regime read on out-of-sample windows that contain a sharp volatility expansion, where volatility-read lag and regime whipsaw concentrate the worst outcomes.

Sources

Method definition (internal strategy taxonomy).Acceptance criteria (internal strategy taxonomy).