The Put-Skew Regime Archetype: how a model reads the price of fear, and why it mostly stands aside

It reads the options market's cost of downside protection rather than the price path, and takes a directional stance only when a second options read corroborates the first; the rest of the time it stays flat.

Method archetype

Protection is not free. In any market with options, someone is always quoting a price to insure against a fall and a price to bet on a rise, and those two prices are rarely the same. When insuring against a fall costs far more, that gap is the crowd putting a price on its own worry. This archetype reads that priced worry, not the path of the underlying.

What separates a put-skew-regime model from a simple fear gauge is what it does with that reading. It does not buy or sell the moment protection looks dear. It treats the price of fear as one of two options-market reads, standardizes each against its own history, and takes a position only when the two agree. Most of the time they do not, and the method stays out. The sections below describe that machinery, read for read and gate to gate, rather than telling a story about why the market moved.

What the method reads

The inputs come from the options market, not the price chart. The first is the cost of downside protection: how richly the market is pricing insurance against a fall, relative to the cost of betting on a rise. The second is a confirming options read that either points the same way as the first or does not. A put-skew-regime model is built on these positioning reads, which is structure the spot price alone cannot show.

The first read is the price of downside protection: dear protection means the crowd is paying up to be insured, and the lean is defensive.

The second read is a separate options signal whose only job is to agree or disagree with the first. Agreement is what the method waits for.

How it decides: the regime gate

Here is the mechanism the older framing skips. Neither read opens a position on its own. The two reads must point the same way at the same time, and the combined reading must be stretched far enough versus its own history to clear a conviction bar. When both conditions hold, the gate opens and a directional stance is taken. When they do not, the method returns to flat and waits. This is decision plumbing, a read feeding a gate feeding a stance, not a forecast of where the underlying is headed.

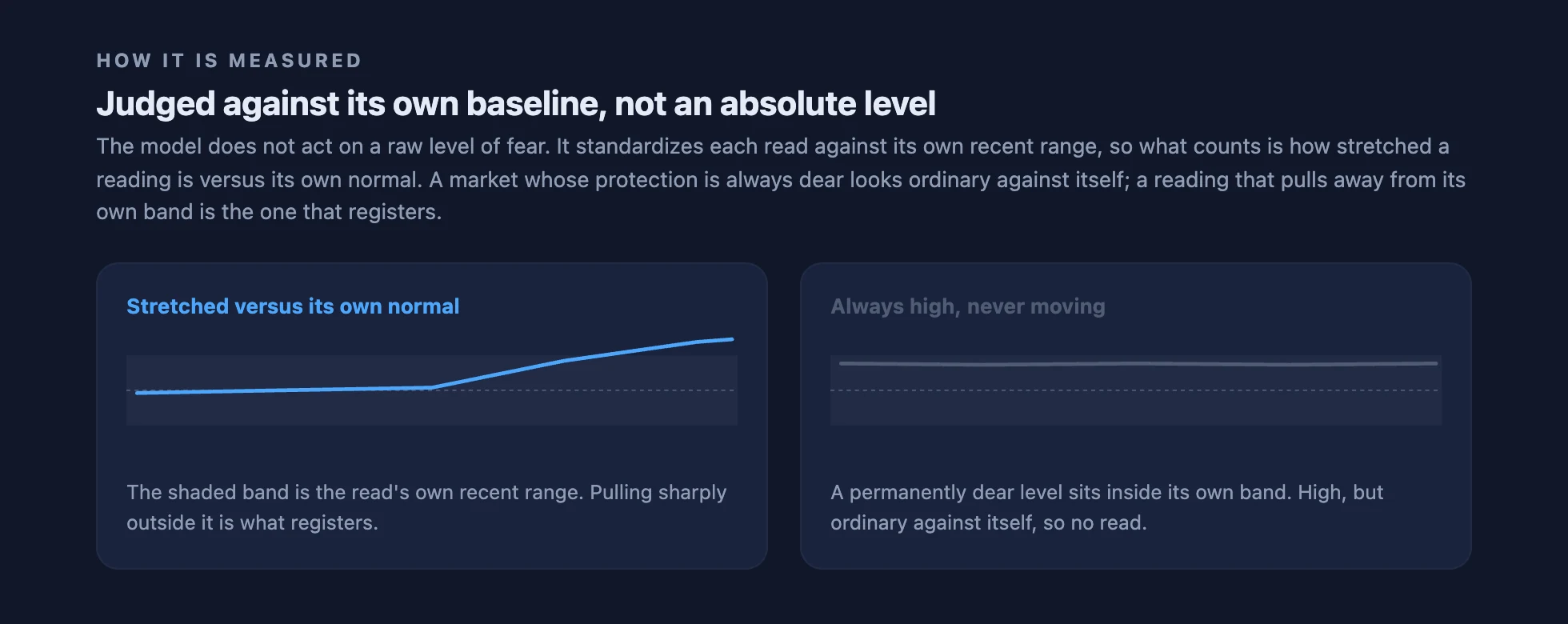

Measured against its own baseline

The method does not act on a raw level of fear. It standardizes each read against its own recent range, so what counts is how stretched a reading is versus its own normal rather than how high it is in absolute terms. A market whose protection is always dear looks ordinary when measured against itself and produces no read. A reading that pulls sharply away from its own band is the one that registers.

Why the read is relative, not absolute

Two markets can both look fearful in absolute terms while only one is sending a signal. Judging each read against its own history is what stops a structurally nervous market from looking like a permanent trade. It also means a level that has been high for a long time is treated as quiet, because against its own baseline it is no longer unusual.

A dear reading alone is not a stance

An elevated price of protection is where most fear reads stop and act. This one does not. A dear reading on its own may be overdone, the crowd paying for a fall that will not come, so the method holds. Only when the second read corroborates the first does it treat the stress as earned and lean with it. That corroboration step is the difference between a disciplined regime read and a reflexive bet against fear.

| The reading | What it means | The stance |

|---|---|---|

| Protection dear, not corroborated | The fear may be overpriced; the second read does not back it | Stand aside |

| Protection dear, corroborated | The stress is treated as earned; both reads point the same way | Lean with it |

| The reads diverge or go quiet | No regime to act on | Flat |

Three states, and bounded risk

The output is one of three states. When the gate opens, the method takes a directional lean, long or short, in the direction the aligned reads imply. When the gate is closed, it holds nothing. A lean is never open-ended: every position is bounded in advance, closing at whichever comes first of a profit-target, a stop-loss, or a maximum-hold timeout. After a position opens the management is mechanical, not a matter of judgement.

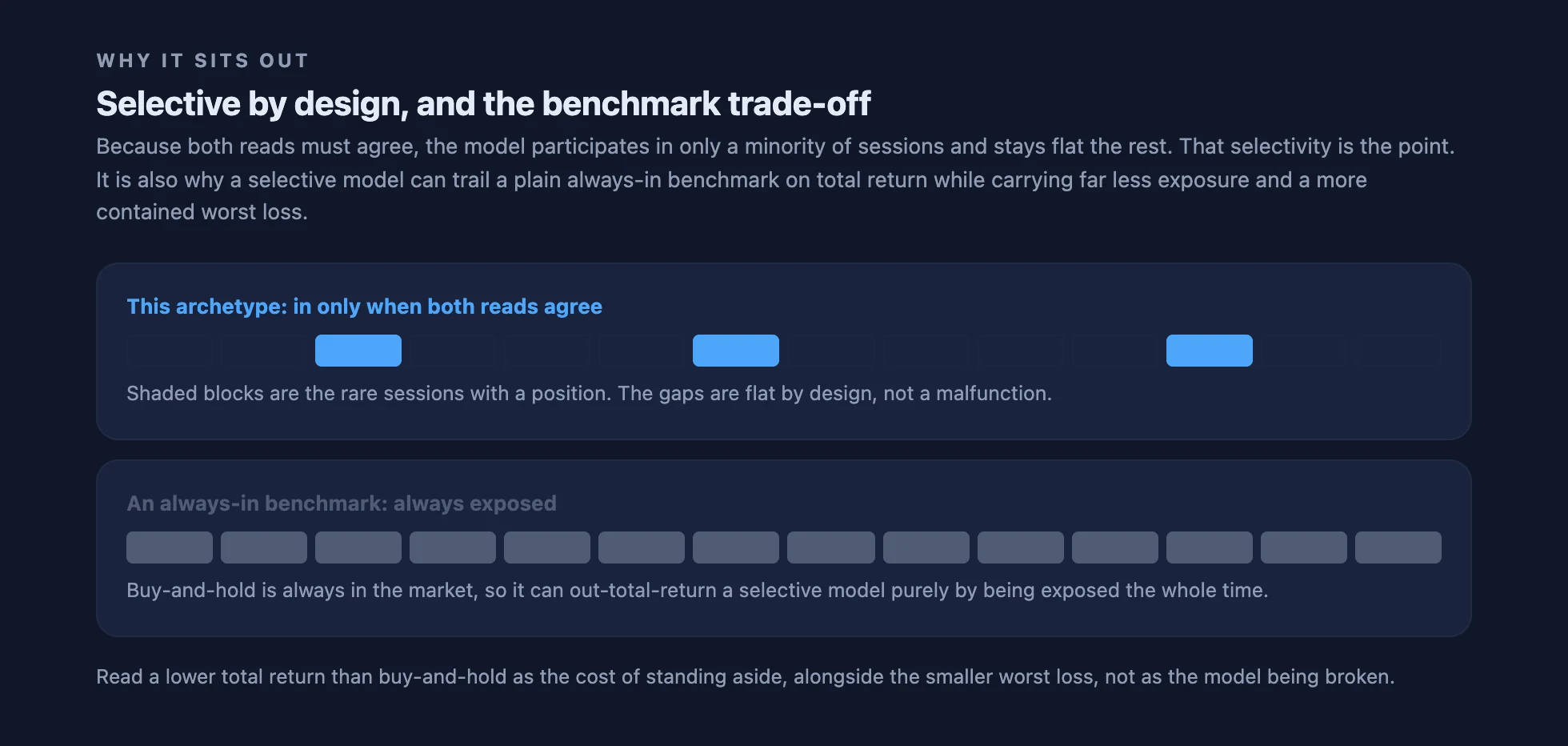

Selective by design

Because both reads must agree, the method participates in only a minority of sessions and stays flat the rest. That selectivity is the point, not a flaw, and it has a consequence worth stating plainly. A model that is in the market only occasionally can trail a plain always-in benchmark on total return, simply because the benchmark is exposed the whole time. The selective model carries far less exposure and, with it, a more contained worst loss.

How to read it on the dashboard

How it earns its place

A model of this archetype moves along a fixed track before it is trusted. It begins as a hypothesis that the price of protection carries a tradeable bias, is measured on history after costs, and is then replayed on time it was never fit to. That walk-forward stage checks whether the signal reproduces the same moments on unseen data, which is a test of the signal, not a claim about profit. The acceptance gates are shown openly as a scorecard, and a reading that falls short of a gate is surfaced openly as a caution rather than treated as a cleared result.

What this archetype is not

- Not a simple contrarian fear-fade: it does not sell every spike in protection, and it requires a second read to corroborate before any stance.

- Not a raw options-skew chart: it is a regime read built on the price of protection, standardized against its own history and gated, rather than a plot of skew.

- Not a volatility forecast: it does not predict how volatile the market will be; it classifies a positioning regime and reads an implied directional bias.

- Not a recommendation or a signal service: it is a method, and an exemplar model built this way may be an early-stage result with no live capital behind it yet.

- Not a promise of returns: a model built this way can still be wrong, and a stress the options market did not anticipate can produce an outcome outside what was seen.

Specific models built on this archetype, with their benchmarks, are listed in the catalog. The archetype itself is a method, not any one of those models.

This explainer describes a method, not a recommendation, and a model built this way is not a guarantee of future results. It is a disciplined way of reading what the options market is paying to be afraid, acting only when a second read agrees, and standing aside the rest of the time.

Sources

This article is based on Stonewell One research, including backtesting, walk-forward verification, deployment monitoring, and model-risk review.