The Percentile-Regime Archetype: Ranking a Market State to Decide When to Go Long, Short, or Stand Aside

How a reusable method component ranks one market-state input into a percentile band to decide when to take the continuation side, the opposite side, or no position at all

What the percentile-regime archetype is

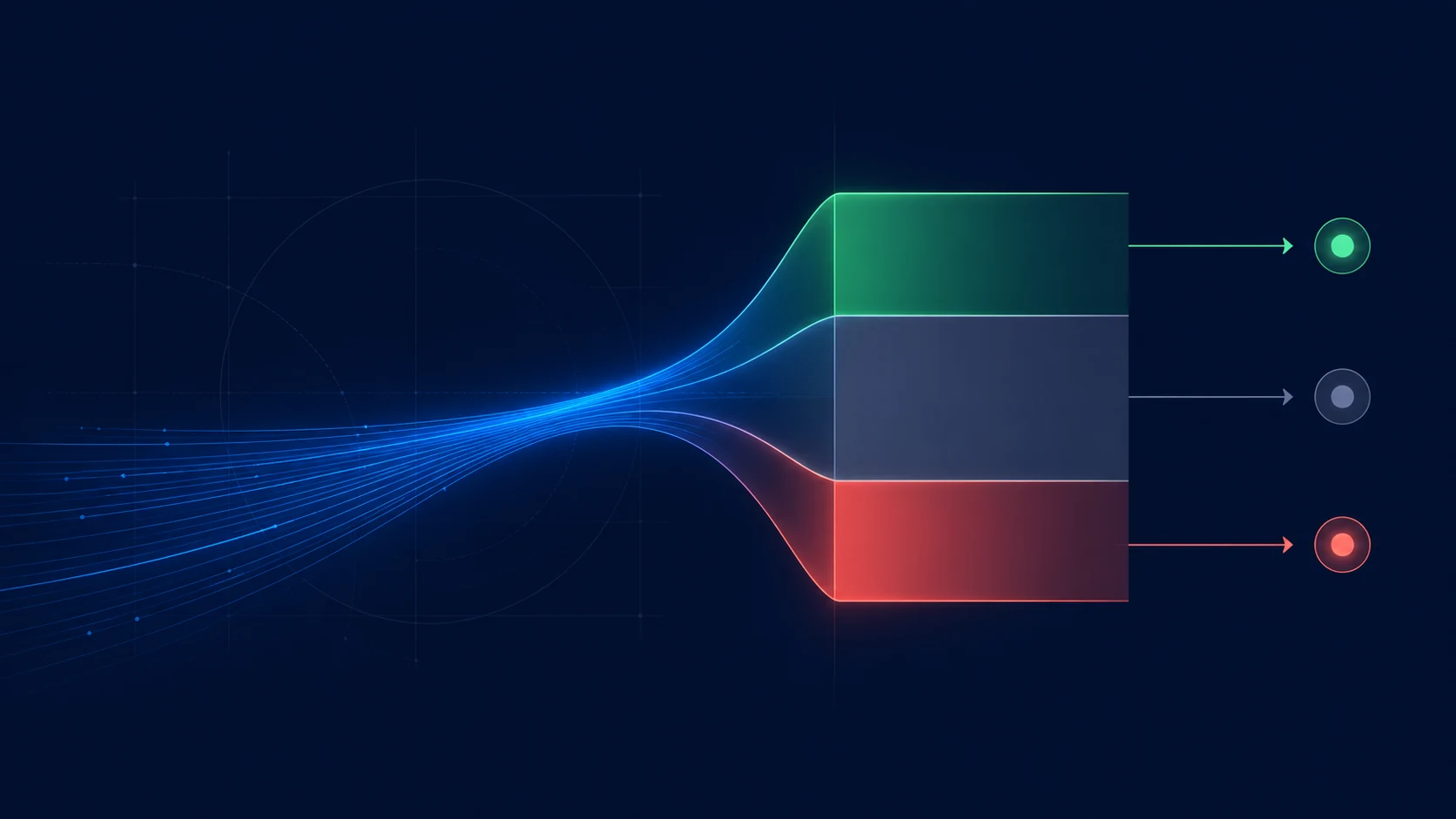

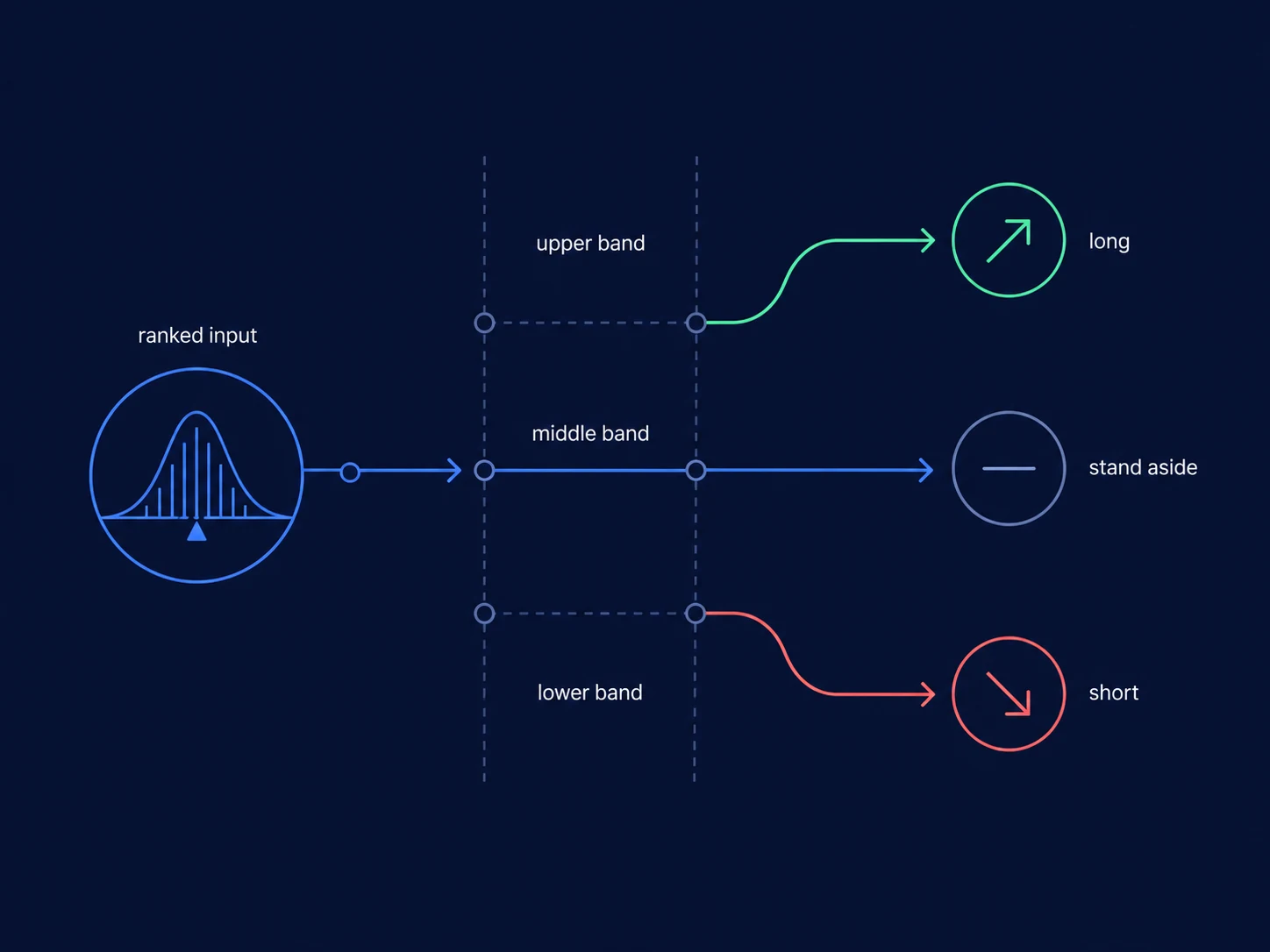

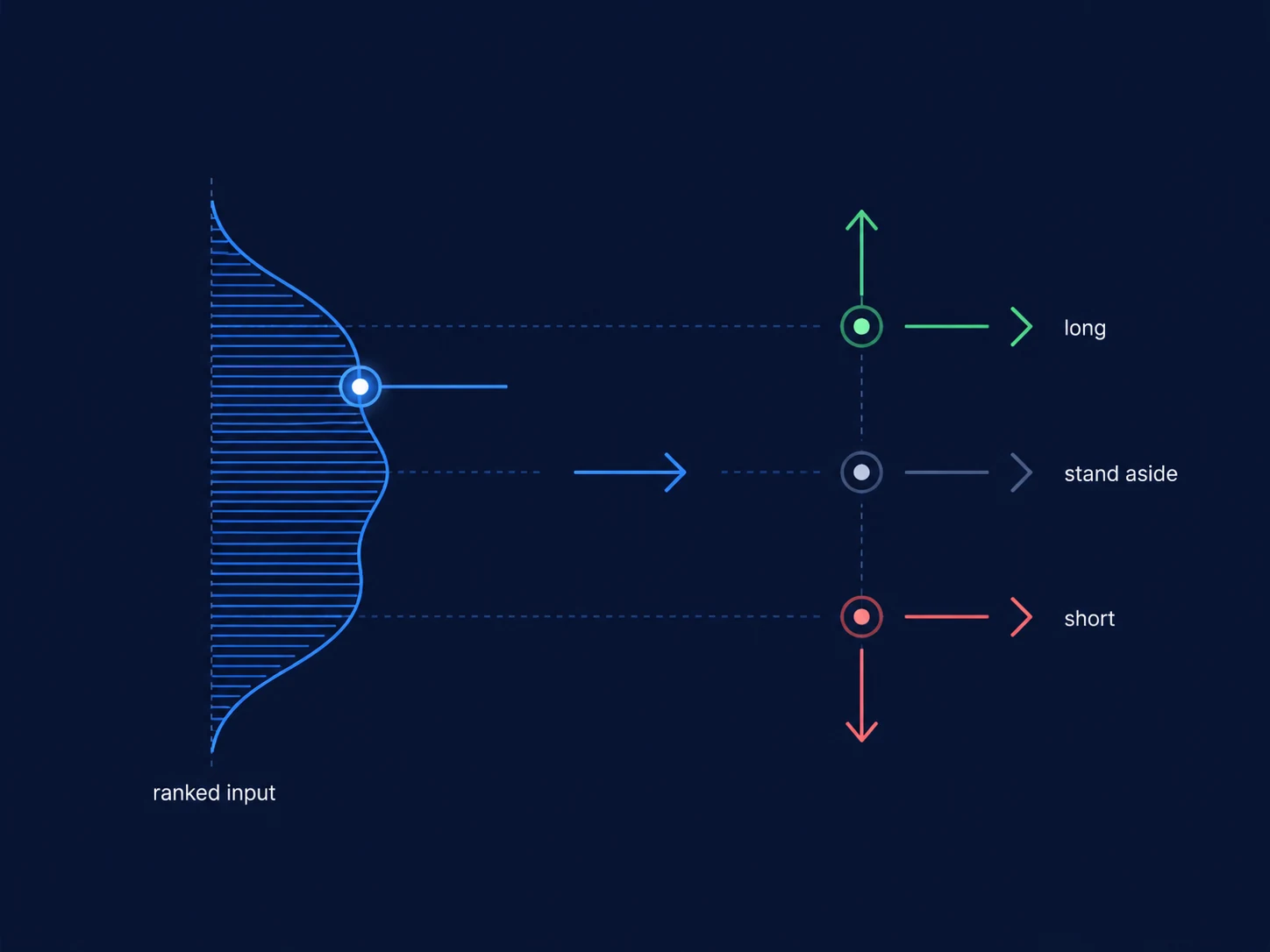

A percentile-regime model is a reusable method component rather than one fixed algorithm. The system takes a single ranked market-state input, scores its current reading against that input's own trailing history, and converts that score into a percentile band. The band, not the raw level and not price itself, is the decision variable. When the ranked reading sits in the upper continuation band the model holds one side; when it sits in the lower band it holds the opposite side; and when it sits in the wide middle band it holds nothing.

This is a deliberately narrow, legible idea, and that narrowness is the point. Any model built from this archetype is doing the same three-state thing, only with a different masked input and different band edges. Throughout this explainer we describe the input only as a ranked market-state reading and never name the underlying column, tenor, or threshold, because those are model internals. The archetype's public contract is the ranking-and-banding mechanism, not the proprietary feature behind it.

> NOTE: This explainer describes a method component in the abstract. It is not a model, not live trading, not a recommendation, and makes no forecast about how any derived model will perform.

> Key takeaways. The percentile-regime archetype is a reusable method component, not a model or a single algorithm: it ranks one masked market-state input against its own trailing history, maps the rank to an upper, middle, or lower band, and takes the continuation side, the opposite side, or no position. It is asset-, symbol-, and model-agnostic, so many models across different markets can be derived from the same component. Any candidate model built from it is judged against the archetype's canonical acceptance bars before it can deploy: minimum thresholds on win rate, total return, and average return per trade, plus a drawdown ceiling and a minimum sample size, and once deployed it is measured against a buy-and-hold benchmark. Everything below describes the component and its backtest methodology; it is not a live model.

Ranking and normalizing a market-state input

The first move is normalization. A raw market-state reading is hard to act on because its scale drifts and its meaning changes with regime. The archetype sidesteps that by ranking today's reading inside a rolling history of its own recent values, producing a percentile score between the lowest and highest readings that history has seen. A reading at the top of its recent range scores near the top of the band; a reading near the middle scores in the middle; an unusually low reading scores near the bottom. Because the score is relative to the input's own recent history, the same mechanism transfers cleanly across very different inputs and very different markets.

How the ranking produces long, short, and flat

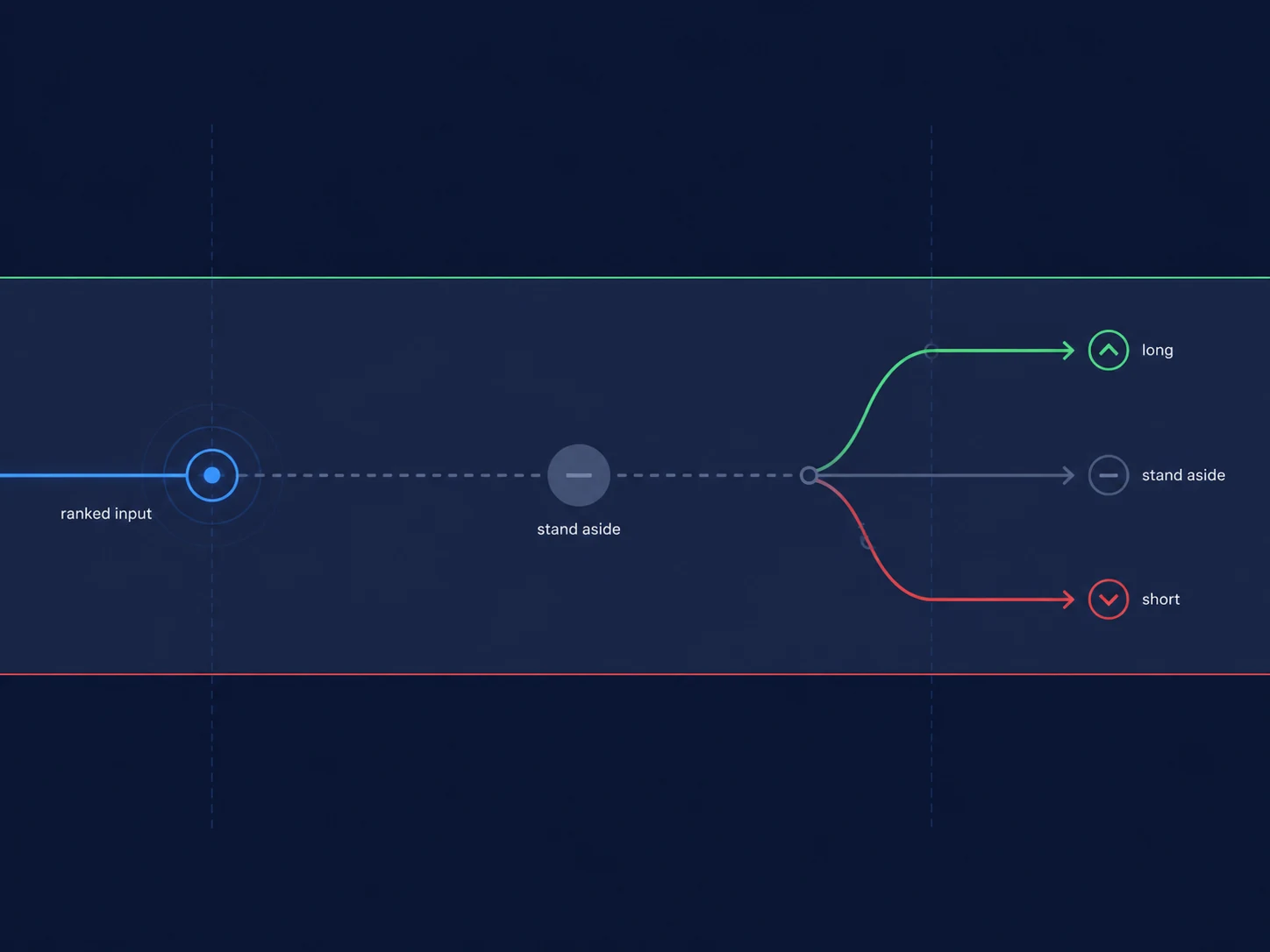

Because the archetype keys off a rank, it is naturally two-sided. A reading that climbs into the top band is treated as one directional state; a reading that falls into the bottom band is treated as the mirror state; the wide middle is treated as no-trade. That is the whole long, short, and flat logic: there is no separate trend filter bolted on, the band assignment is the signal. A single threshold structure produces all three states, which is why the method is cheap to reason about and easy to audit after the fact.

A long-only or short-only system cannot express this. The rank-based design is what lets one rule cover both directions, and which direction dominates is a property of the chosen input and window, not of the archetype itself.

Horizon and regime fit

The archetype does not read price directly; it reads where a market-state input sits in its own distribution, then positions in price. Two consequences follow. First, entries cluster at band edges: the model commits as the ranked reading crosses into a band, not at any particular price level. Second, its price impact is indirect: it expresses a view about the state the market is in and lets price catch up, rather than reacting to a raw price move. When the ranked reading is mid-distribution, the model is flat regardless of what price is doing.

Because the band is computed against trailing history, the natural horizon of any model built this way is inherited from how slowly its chosen input moves through its own range. A slow-moving input produces a slow-cadence model; a fast-moving input produces a faster one. The archetype itself fixes no horizon; it is a method component that adapts its cadence to the input it is given.

Signal generation

Signal generation is a deterministic function of the rank. The current reading is ranked, the rank is mapped to a band, and the band is mapped to a target position. There is no separate scoring model layered on top: the percentile score is the signal. This keeps the path from observation to action short enough to trace by hand, which is what makes models of this archetype straightforward to monitor and to fault-find.

Position behaviour and lifecycle

A position in this archetype has a simple lifecycle: it opens when the ranked reading crosses into a directional band, it is held while the reading stays in that band, and it closes on one of three events (a take-profit, a stop-loss, or the reading leaving the band, which is a signal exit), with a timeout as a backstop. The exit type is therefore informative about which path ended a position, and, for any model built from the archetype, the mix of exit types is a compact summary of how that model actually behaved.

Risk controls

Risk control in this archetype is expressed through method constructs rather than discretion. The stand-aside state is the first control: whenever the ranked reading sits in the neutral middle band, the model holds no position, so risk is simply not taken through the large middle of the range. On open positions, three exit constructs bound the outcome: a stop-loss caps the loss, a take-profit books the gain, and a signal exit closes the position when the ranked reading leaves the band that justified it. A timeout serves as a backstop so no position is held indefinitely. These are structural controls baked into the mechanism, not parameters tuned after the fact.

Why the archetype stands aside

Standing aside is a first-class state, not an afterthought. Whenever the ranked reading sits in the neutral middle band, a percentile-regime model holds no position. This is the mechanism's built-in humility: it only commits at distributional extremes and is content to be flat through the large middle of the range, which is why models of this archetype can spend meaningful stretches out of the market. A reader evaluating any percentile-regime model should expect, and want, long flat periods; constant exposure would mean the band edges were set too tight.

Failure modes

Two failure modes follow directly from the mechanism. First, band-edge whipsaw: when the ranked reading hovers around a band boundary it can cross back and forth, opening and quickly closing positions and paying an edge cost each time. Second, lag after a sharp state break: because the band is computed against trailing history, a fast change can leave the reading mid-band while price has already moved, so the model stands aside through part of the move and commits late. Both failure modes are inherent to the design, which means they should be measured and tolerated, not engineered away by overfitting the band edges to one window.

Why it is reusable across assets, symbols, and models

The reason this archetype is a component and not a one-off is that its decision logic is independent of the input it consumes. Because every reading is normalized into a percentile of its own history before any decision is made, the same ranking-and-banding mechanism can be pointed at completely different market-state inputs, across completely different assets and symbols, to derive many distinct models. Each derived model inherits the same three-state contract (continuation band, opposite band, neutral middle) while differing only in its chosen input and band edges. One component, many models: that reuse is the whole reason the archetype is defined separately from any model built from it.

Volatility as the ranked input

A useful concrete case is when the input being ranked is volatility itself. Instead of ranking a market-state level, a model built this way first turns the watched reading into a rolling measure of how much it has recently moved, and then ranks that volatility measure against its own trailing history in exactly the way described earlier. A high band means recent volatility sits near the top of its own range, a low band means it sits near the bottom, and the wide middle is ordinary volatility. The machinery is unchanged: the same ranking against recent history, the same three history-derived bands, and the same first-class flat state across the broad middle.

One structural difference is worth naming. In the base case the band a reading occupies tends to imply the side on its own. A volatility reading has no inherent up or down, so when volatility is the ranked input the band marks a regime, an unusually turbulent stretch or an unusually calm one, rather than a direction. A model built this way reads that volatility regime from the band and sets its side together with a separate directional read, while still standing aside whenever volatility rests in its ordinary middle range. The ranking decides when the reading is unusual enough to act; the side is supplied alongside it rather than by the volatility level itself.

Selecting a model of this archetype

A model built from the archetype is only a candidate until it clears a generic set of acceptance criteria. The same canonical bars apply to every model of this archetype: a minimum win rate, a minimum total return, a minimum average return per trade, a maximum drawdown ceiling, and a minimum sample size. These are selection criteria for any model of this shape, not the record of any one model; a candidate that misses them does not clear review for deployment. The archetype defines how a model decides; these bars define whether a given model is good enough to use.

Where the band edges come from

The band edges are the only real tuning surface the archetype exposes. Pushing the continuation and opposite edges toward the extremes makes the model more selective and keeps it flat more often; pulling them toward the middle makes it commit more readily and trade more often. Because the edges are expressed as percentiles of the input's own history rather than as absolute levels, the same edge settings keep their meaning even as the underlying reading drifts in scale. Setting the edges too tight is the classic overfit: it manufactures a smooth-looking history that will not survive a new window.

What the archetype deliberately omits

Much of the archetype's value is in what it leaves out. There is no trend overlay, no volatility filter, no regime classifier sitting on top of the percentile decision, and no discretionary override. Each omission is a design choice that keeps the path from observation to position auditable. Anything that cannot be expressed as a band of the ranked input is, by construction, outside the archetype. A model that needs those extra inputs is a different archetype, not a tuned version of this one.

How to read a model built from it

When you evaluate a model derived from this archetype, read it through the mechanism rather than through a single headline outcome. Ask which band each position came from, how often the reading sat in the neutral middle, and which exit construct ended each position. Those three questions reconstruct the model's behaviour directly from the method, without needing any narrative about why a market moved. The archetype gives every model a common, legible vocabulary for that kind of review.

Archetype is not a symbol or a model

The archetype names how a model decides (rank a state input, band it, trade the band), not how any given model behaves over time, and not which market it trades. A model's behaviour label (trend, transitional, mean-reversion) and its horizon (short, medium, long) are assigned per model from observed results, later; they are not inherited from the archetype. Two percentile-regime models on different inputs could land in completely different behaviour labels while sharing the identical decision mechanism. The archetype is the reusable component; symbols and models are what you derive from it.

> How much to rely on a model of this archetype. Everything here describes a method and its backtest methodology, evaluated gross of commission and slippage, so net-of-cost results would be lower. No model is live by default, and a candidate is not trustworthy on an in-sample backtest alone: it must survive out-of-sample / walk-forward validation and clear the acceptance gates before it can deploy. Treat any single backtest as evidence about the method's mechanics, not a guarantee of future results; the main limitation is that a trailing-window rank lags a fast regime break, so caution is warranted around sharp state changes.

Conclusion

The percentile-regime archetype is a single-input, three-state method component: rank a market-state reading against its own history, band it, and go long, short, or flat accordingly. Its strengths (a built-in stand-aside state and naturally two-sided positioning) and its weaknesses (band-edge whipsaw and lag after sharp breaks) both fall straight out of that mechanism. Because the decision logic is independent of the input it reads, the same component derives many models across many assets and symbols, each judged on its own against the canonical acceptance bars.

Key Takeaways

• The decision variable is a percentile band of a ranked market-state input: continuation band long, opposite band short, middle band flat.

• The method is two-sided by construction; one threshold structure produces long, short, and flat states.

• Standing aside in the neutral band is a designed risk control, not a gap.

• Band-edge whipsaw and trailing-window lag are the archetype's characteristic failure modes.

• An archetype is the reusable component from which symbols and models are derived; it is not itself a symbol or a model.

Next Steps and Further Research

• Derive and compare several models from this archetype to separate archetype-wide behaviour from model-specific behaviour.

• Treat behaviour label and horizon as a per-model classification step, assigned from each model's observed results.

• Capture the band-edge whipsaw rate as a standard diagnostic for every model built from this archetype.

Sources

This article is based on Stonewell One research, including backtesting, walk-forward verification, deployment monitoring, and model-risk review.